Gin consumption declined, but it’s not that simple.

Less gin was sold last year than in the previous year and it’s the first time I’ve seen a downwards trending pattern for the category since my first trend report in 2011.

According to the CGA, value dropped by 23% and volume dropped by 28% in the 12 months up to October 2021.

Shrinking numbers is hardly a surprise given the pandemic continued well into last year and with it, many of the routes to market ground to a halt for months on end. It's also true that the decline is likely to be a temporary lapse and it’s safe to assume that there will be some form of, if not a massive bounce back in 2022.

The rampant growth of gin elsewhere around the world boding well for future exports aside, even anecdotal indicators point towards a likely return to form within these shores. Namely, the number of UK gin distilleries grew by 110 last year, meaning there are now 820 UK gin distilleries according to the Office for National Statistics.

The concern I have isn’t the overall numbers, it’s that comparatively speaking Gin seems to have performed far worse than any other category. Whisky and Rum figures are not that bad, while Tequila's were positive (over 1.5 million bottles of tequila were sold in Britain in the 12 months to 11 September, up 36% on the same period the year before).

Over on Amazon, gin only grew by 1% in 2021 (compared to vodka which was up 28.2% on the previous year, Rum up 26.1% and Cognac 23.5%). It also saw the greatest decrease in price of 4.3%, ahead of the wider average price fall for spirits sold on that platform, which was around 1.4% year-on-year.

So why did this under performance happen? Gin fatigue amongst drinkers is often quoted, and seemingly with no sense of irony - people drinking the proliferation of gin bottles now on their shelves (rather than buying more booze full stop) during the second lockdown another.

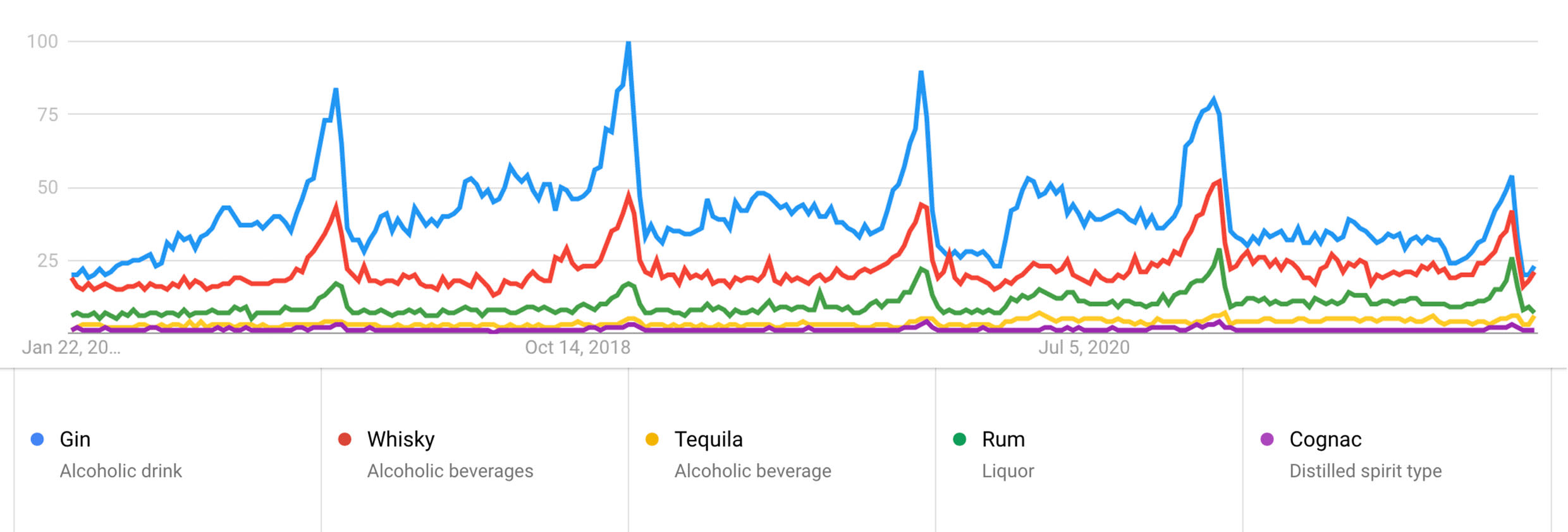

Two opposites can’t both be true, and if you probe further you’ll find neither hold much weight. The gin fatigue argument doesn’t wash when you see that the consumption in bars, restaurants and pubs was proportionately up on previous years when trade returned last year. This is further dispelled when one considers that the biggest spirits related products last Christmas is a snow globe shaped gin liqueur. Meanwhile, even a hasty look on Google search data shows that gin and gin cocktails over index in the UK (even if by a smaller amount as in previous years).

Like it or hate it but Gin is still trending above and beyond other categories.

A beleaguered group of Micro-distilleries.

If not consumer interest or a reticence to spend money on booze – then what else could it be at the route of such a decline compared to others?

I think the prevalence of young, small distilleries with underdeveloped routes to market had a far greater impact on gin in particular than many want to acknowledge. Combine this with the fact that the bulk of mid-sized gin brands here in the U.K. are imported and you have two significant factors at play – even if it’s going un-reported from other analysts to date.

Take the former; according to the Office for National Statistics, British Micro distilleries with less than 10 employees now make up 730 businesses – some 90% of the total producers. Many of these new (less than three-year-old) brands didn’t have much cash flow at the best of times, let alone reserves to operate in a pandemic or invest in growth opportunities that presented themselves.

Almost none were in the big grocers or wholesalers, so by taking away the few bars and local shops the “trade” portion of their business was culled overnight. The reality is that few had built enough of a reputation to find digital retailers who were willing to take them on once it all began too…

It’s true that the elite section of small producers found ways to sell direct to consumers, and that many have since reported that while their volume was way down, margin was up cumulating in a net even result. That wasn’t the case for most though. Many gin producers didn’t have the luxury of weathering the storm so resorted to short term solutions that might have worked had the pandemic been a few months, but not close to 2 years.

Unfortunately, short term solutions end up falling short compared to those with a longer-term vision and a proper strategy. Gin producers over-index in the group that resorted to that approach as they over-index in the group of smaller, less funded producers operating in the Uk.

Worse still is that there is a huge amount of small to mid-sized players who are stuck in the loop of short-term thinking and month by month solutions. This has left a once thriving but now beleaguered group of micro-distillers struggling to create meaningful growth compared to other categories, like Scotch, whose strategies are all coming to fruition.

Meanwhile, many foreign gin brands stopped campaigns and promos as most gear them heavily towards the on-trade (bars, restaurants). This is understandable given there were fears about import logistics / their own distributors and agents on furlough / the financial resilience of wholesalers etc. playing out across the global freight network.

Dozens of established brands made across Europe, Australia and elsewhere decided to not push through stock already in the UK and allow organic sales to turnover, a wise move given the logistical pile up that Covid + Brexit have since wrought on the supply chain.

While the same could be said for Rum, Tequila and Whisky brands, the differentiator for why Gin underperformed could be down to the fact that most are still not active in the UK market today and are waiting until later this year to begin campaigns once more. Internationals in other categories seem to have kicked back to life already.

Flavoured Gin churns as much as it grows.

Another reason for the languid performance is the Flavoured Gin segment. So much of gin’s growth has relied on the boom happening in the flavoured sector. Irrespective of the reason for it – Flavoured Gin faltering equates to a big drop for the category as a whole.

In recent years Beefeater Blood Orange and Pink have grown into best sellers, Beefeater Dry has not shared that trajectory - in fact, it’s been overtaken by Hendrick’s. The UK’s best-selling gin is Gordon’s Pink, not Gordon’s. Tanqueray Flor De Sevila is now a top 10 brand by volume. Flavoured Gins make up most of the biggest selling variants and it’s clear that without its success, Gin as a whole would have long been relegated to a trend of the past.

But (and it’s a big BUT) what’s being left unsaid is that between those names alone there’s been a dozen unsuccessful releases that have come and gone - literally.

Halewood alone must have launched and culled two dozen. Bombay Bramble seems to have had a bumpy ride of late and don’t get me started on the merry-go-round of mediocrity going on in supermarket home ranges. Flavoured Gin churns as much as it expands and for every hit there are numerous duds. It’s a volume game where chucking as many things against the wall and seeing what sticks is what has led to the genre’s success. It's also seemingly the way some approach recipe development given the taste, but that’s another story. With fewer releases, there have been far fewer successes.

Combine that with the majority’s finite “sell by” date in terms of interest and buzz. To date, despite triple digit starts there are few that have sustained their meteoric early rise. It’s another reason why so many launch new line after another - it’s all transient shades replacing each other in a kaleidoscope of novelty until one goes stratospheric.

The reduced NPD in that sector of Gin throughout 2020 may well have played a key role for the stagnating sales overall in 2021. It turns out that what category experts have said for years – there are very few flavoured gins that get repeat sales and even fewer that have loyal audiences who stick to just one brand – is true. Consumers move from one to the next in a constant state of exploration.

The multinationals ensured their repeat sales due to their incredibly low-price points but elsewhere, the zeitgeist moved and moved and it may well have been the case that 2021 was the year that many of the brands that once had a bit of buzz simply fizzled out. With less coming down the gin bandwagon droves of drinkers may well have moved to other categories for their hit of new and exciting.

Is there a silver lining in the decline?

Big boys dominating the groceries, limited NPD in the flavoured sector, smaller operations not having a diverse and robust route to market and a lack of financial infrastructure at a micro-distillery level (and indeed a lack of finance) each created issues. Short term solutions leading to short term results, as well as internationals who stopped their marketing in the UK also caused a negative impact. Overall, it’s a complex web that lead to a serious decline in volume.

Whichever way you weigh it and whatever other factors you want to layer on-top - it’s also clear that years of rampant growth have papered over major fracture points for the category and the Uk's craft distilling sector.

But that’s where I can see the silver lining in Gin’s “over-decline”. So much of it is temporary and so many of the reasons behind why it’s done terribly (comparatively) is exactly what makes it so exciting a spirit.

Small operations are the large majority of operations – meaning despite gin makers having been especially hard hit, almost all have survived. That bodes well for when they do eventually recover as it keeps the scene dynamic and diverse.

The lack of NPD over the past two years is good as it means there’s now a glut of ideas emerging along with a renewed focus on quality.

The need to diversify business models, consolidating routes to market and build more robust fiscal infrastructure will lead to a better equipped and more resilient craft distilling industry – most of whom are primarily gin makers.

Yes, Gin took a shellacking. More than any other spirit category in the UK and the overall numbers look dire. But it’s also been made stronger. It is emerging in a very strong place and with the potential to bounce back far bigger than it was and continue growing for the next 3-5 years.

For a category that would likely have faced a slow decline and never addressed some of the issues above until it was too late had there not been a pandemic - that’s something to be very optimistic about in the year ahead.